Introduction to Predictive Modeling: Regressions

Regressions

offer a different approach to prediction compared to decision trees.

Regressions, as parametric models, assume a specific association structure

between inputs and target. By contrast, trees, as predictive algorithms, do not

assume any association structure; they simply seek to isolate concentrations of

cases with like-valued target measurements.

The

regression approach to the model essentials in SAS Enterprise Miner is outlined

over the following pages. Cases are scored using a simple mathematical prediction formula. One of several

heuristic sequential selection

techniques is used to pick from a collection of possible inputs and creates a

series of models with increasing complexity. Fit statistics calculated from

validation data select the optimal

sequence model.

Regressions predict cases using a mathematical

equation involving values of the input variables.

In standard

linear regression, a prediction estimate for the target variable is formed from

a simple linear combination of the inputs. The intercept centers the range of

predictions, and the remaining parameter estimates determine the trend strength

(or slope) between each input and the target. The simple structure of the model

forces changes in predicted values to occur in only a single direction (a

vector in the space of inputs with elements equal to the parameter estimates).

Intercept and parameter

estimates are chosen to minimize the

squared error between the predicted and observed target values (least squares

estimation). The prediction estimates can be viewed as a linear approximation

to the expected (average) value of a target conditioned on observed input

values.

Linear

regressions are usually deployed for targets with an interval measurement

scale.

Logistic regressions are closely related to linear regressions.

In logistic regression, the expected value of the target is transformed by a link function to restrict its value to the

unit interval. In this way, model predictions can be viewed as primary outcome

probabilities. A linear combination of the inputs generates a logit score, the log of the odds of

primary outcome, in contrast to the linear regression's direct prediction of

the target.

The presence of

the link function complicates parameter estimation. Least squares estimation is

abandoned in favor of maximum likelihood estimation. The likelihood function is

the joint probability density of the data treated as a function of the

parameters. The maximum likelihood estimates the values of the parameters that

maximize the probability of obtaining the training sample.

If your interest is ranking predictions,

linear and logistic regressions will yield virtually identical results.

For binary prediction, any monotonic function that

maps the unit interval to the real number line can be considered as a link. The

logit link function is one of the

most common. Its popularity is due, in part, to the interpretability of the

model.

There are two equivalent ways to interpret a

logistic regression model. Both relate changes in input measurements to changes

in odds of primary outcome.

An

odds ratio expresses the increase in primary

outcome odds associated with a unit change in an input. It is obtained by

exponentiating the parameter estimate of the input of interest.

A

doubling amount gives the amount of change required for doubling the primary

outcome odds. It is equal to log(2) ≈ 0.69 divided by the parameter

estimate of the input of interest.

If the predicted logit scores remain in

the range -2 to +2, linear and logistic regression models of binary targets are

virtually indistinguishable. Balanced

sampling (Chapter 7) often ensures this. Thus, the prevalence of balanced

sampling in predictive modeling might, in fact, be a vestigial practice from a

time when maximum likelihood estimation was computationally extravagant.

To demonstrate the properties of a logistic

regression model, consider the two-color prediction problem introduced in

Chapter 3. As before, the goal is to predict the target color, based on

location in the unit square.

The predictions can be decisions, rankings, or

estimates. The logit equation produces a ranking or logit score. To get a

decision, you need a threshold. The easiest way to get a meaningful threshold

is to convert the prediction ranking to a prediction estimate. You can obtain a

prediction estimate using a straightforward transformation of the logit score,

the logistic function. The logistic

function is simply the inverse of the logit function.

Parameter estimates are obtained by maximum

likelihood estimation. These estimates can be used in the logit and logistic

equations to obtain predictions. The plot on the right shows the prediction

estimates from the logistic equation. One of the attractions of a standard

logistic regression model is the simplicity of its predictions. The contours

are simple straight lines. (In higher dimensions, they would be hyperplanes.)

This enables a straightforward interpretation of the model using the odds

ratios and doubling amounts shown at the bottom left. Unfortunately, simplicity

can also lead to prediction bias (as scrutiny of the prediction contours

suggests).

The

last section of this chapter shows a way to extend the capabilities of logistic

regression to address this possible bias.

To score a new

case, the values of the inputs are plugged into the logit or logistic equation.

This action creates

a logit score or prediction estimate. Typically, if the prediction estimate is

greater than 0.5 (or equivalently, the logit score is positive), cases are

usually classified to the primary outcome. (This assumes an equal

misclassification cost. See Chapter 7.)

While the prediction formula would seem to be the

final word in scoring a new case with a regression model, there are actually

several additional issues that must be addressed.

What

should be done when one of the input values used in the prediction formula is

missing? You might be tempted to simply treat the missing value as zero and

skip the term involving the missing value. While this approach can generate a

prediction, this prediction is usually biased beyond reason.

How do you score cases with unusual values?

Regression models make their best predictions for cases near the centers of the

input distributions. If an input can have (on rare occasion) extreme or outlying

values, the regression should respond appropriately.

What value should be used in the prediction

formula when the input is not a number? Categorical inputs are common in

predictive modeling. They did not present a problem for the rule-based

predictions of decision trees, but regression predictions come from algebraic

formulas that require numeric inputs. (You cannot multiply marital status by a

number.) A method to include nonnumeric data in regression is needed.

What happens when the relationship between

the inputs and the target (or rather logit of the target) is not a straight

line? It is preferable to be able to build regression models in the presence of

nonlinear (and even non-additive) input target associations.

The above

questions are presented as scoring-related issues. They are also problems for

model construction. (Maximum likelihood estimation requires iteratively scoring

the training data.) The first of these, handling missing values, is dealt with

immediately. The remaining issues are addressed, in turn, at the end of this

chapter.

The default

method for treating missing values in most regression tools in SAS Enterprise

Miner is complete-case analysis. In complete-case analysis, only those

cases without any missing values are used in the analysis.

Even a smattering

of missing values can cause an enormous loss of data in high dimensions. For

instance, suppose that each of the k

input variables is missing at random with probability a. In this situation, the expected proportion

of complete cases is as follows:

Therefore, a 1%

probability of missing (a=.01) for 100 inputs leaves only 37% of the

data for analysis, 200 leaves 13%, and 400 leaves 2%. If the missingness

were increased to 5% (a=.05), then <1% of the data would be

available with 100 inputs.

The purpose of

predictive modeling is scoring new cases. How would a model built on the

complete cases score a new case if it had a missing value? To decline to score

new incomplete cases would be practical only if there were a very small number

of missing values.

Missing values arise for a variety of

reasons. For example, the time since last donation to a card campaign is

meaningless if someone did not donate to a card campaign. In the PVA97NK data set, several demographic inputs have

missing values in unison. The probable cause was no address match for the

donor. Finally, certain information, such as an individual's total wealth, is

closely guarded and is often not disclosed.

Missing value

replacement strategies fall into one of two categories.

Synthetic distribution methods use a one-size-fits-all approach to

handle missing values. Any case with a missing input measurement has the

missing value replaced with a fixed number. The net effect is to modify an

input's distribution to include a point mass at the selected fixed number. The

location of the point mass in synthetic distribution methods is not arbitrary.

Ideally, it should be chosen to have minimal impact on the magnitude of an

input's association with the target. With many modeling methods, this can be

achieved by locating the point mass at the input's mean value.

Estimation methods eschew the one-size-fits-all approach and

provide tailored imputations for each case with missing values. This is done by

viewing the missing value problem as a prediction problem. That is, you can train

a model to predict an input's value from other inputs. Then, when an input's

value is unknown, you can use this model to predict or estimate the unknown

missing value. This approach is best suited for missing values that result from

a lack of knowledge, that is, no-match or non-disclosure, but it is not

appropriate for not-applicable missing values. (An exercise at the end of this

chapter demonstrates using decision trees to estimate missing values.)

Because

predicted response might be different for cases with a missing input value, a

binary imputation indicator variable is often added to the training data. Adding

this variable enables a model to adjust its predictions in the situation where missingness

itself is correlated with the target.

Managing Missing Values

Managing Missing Values

The

demonstrations in this chapter assume that you completed the demonstrations in

Section 4.1.

As discussed

above, regression requires that a case have a complete set of input values for

both training and scoring.

Right-click the PVA97NK data source and select Explore . from the menu. The

Explore - AAEM.PVA97NK window

opens.

There

are several inputs with a noticeable frequency of missing values, for example, Age and Income Group

There are several ways to proceed:

Do nothing. If there are very few cases with missing values,

this is a viable option. The difficulty with this approach comes when the model

must predict a new case that contains a missing value. Omitting the missing

term from the parametric equation usually produces an extremely biased

prediction.

Impute a synthetic value for the missing value. For

example, if an interval input contains a missing value, replace the missing

value with the mean of the non-missing values for the input. This eliminates

the incomplete case problem but modifies the input's distribution. This can

bias the model predictions.

Making the missing value imputation process

part of the modeling process allays the modified distribution concern. Any

modifications made to the training data are also made to the validation data

and the remainder of the modeling population. A model trained with the modified

training data will not be biased if the same modifications are made to any

other data set that the model might encounter (and the data has a similar

pattern of missing values).

Create a missing

indicator for each input in the data set. Cases often contain missing

values for a reason. If the reason for the missing value is in some way related

to the target variable, useful predictive information is lost.

The missing indicator is 1 when the

corresponding input is missing and 0 otherwise. Each missing indicator becomes

an input to the model. This enables modeling of the association between the

target and a missing value on an input.

To address

missing values in the PVA97NK data set, impute synthetic data values and

create missing value indicators.

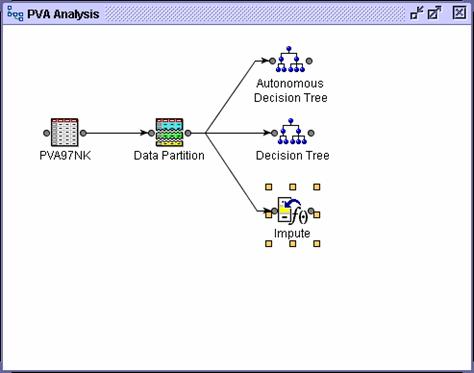

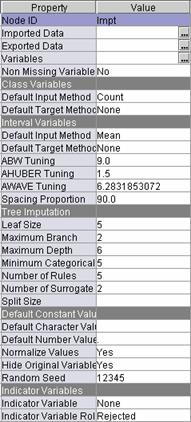

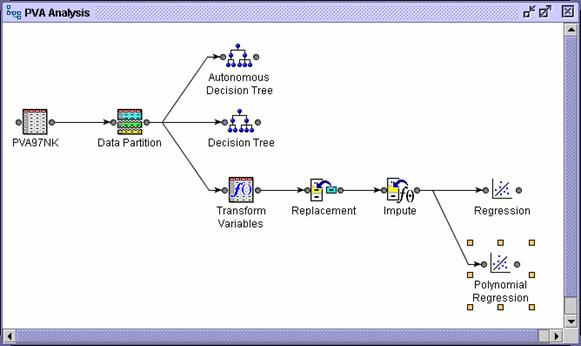

Select the Modify tab.

Drag an Impute tool into the diagram

workspace.

Connect the Data

Partition node to the Impute node.

Select the Impute

node and examine the Properties panel.

The

defaults of the Impute node are as follows:

For interval inputs, replace any missing

values with the mean of the non-missing value

For categorical inputs, replace any missing

values with the most frequent category.

Select Indicator Variable

Unique.

Select Indicator Variable Role

Input.

With

these settings, each input with missing values generates a new input. The new

input named IMP_original_input_name

will have missing values replaced by a synthetic value and nonmissing values

copied from the original input. In addition, new inputs named M_original_input_name will be added to the

training data to indicate the synthetic data values.

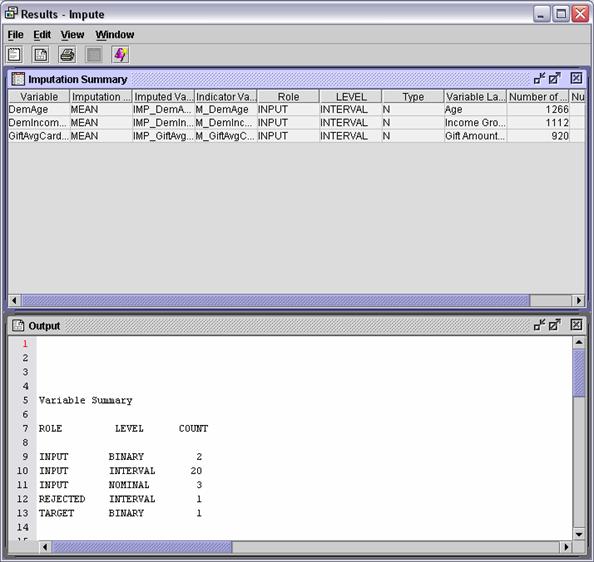

Run the Impute node and review the Results window. Three inputs had

missing values.

With

all missing values imputed, the entire training data set is available for

building the logistic regression model. In addition, a method is in place for

scoring new cases with missing values. (See Chapter 8.)

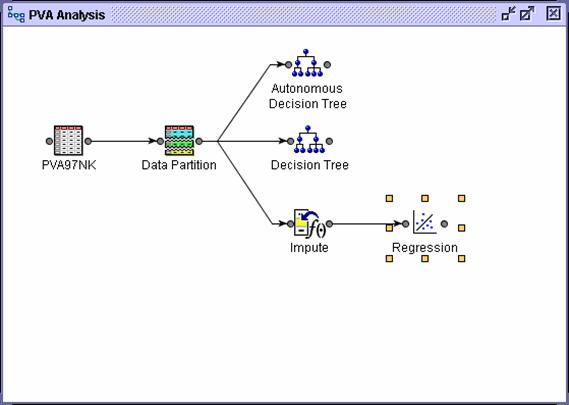

Running the Regression Node

There are several tools in SAS Enterprise Miner to

fit regression or regression-like models. By far, the most commonly used (and,

arguably, the most useful) is the simply named Regression tool.

Select the Model tab.

Drag a Regression tool into the diagram

workspace.

Connect the Impute

node to the Regression node.

The

Regression node can create several types of regression models, including linear

and logistic. The type of default regression type is determined by the target's

measurement level.

Run the Regression

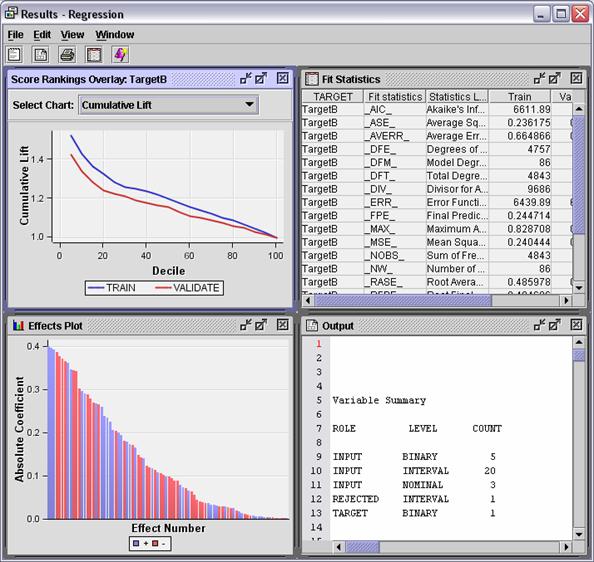

node and view the results. The Results - Regression window opens.

Maximize the Output

window.

Lines

5-13 of the Output window summarize the roles of variables used (or not) by the

Regression node.

ROLE LEVEL COUNT

INPUT BINARY 5

INPUT INTERVAL 20

INPUT NOMINAL 3

REJECTED INTERVAL 1

TARGET BINARY 1

The

fit model has 28 inputs that predict a binary target.

Lines 45-57 give more information about the model, including the

training data set name, target variable name, number of target categories, and

most importantly, the number of model parameters.

Training Data Set EMWS2.IMPT_TRAIN.VIEW

DMDB Catalog WORK.REG_DMDB

Target Variable TargetB (Target Gift Flag)

Target Measurement Level Ordinal

Number of Target Categories 2

Error MBernoulli

Link Function Logit

Number of Model Parameters 86

Number of Observations 4843

Based on the

introductory material on logistic regression that is presented above, you might

expect to have a number of model parameters equal to the number of input

variables. This ignores the fact that a single nominal input (for example, DemCluster) can generate scores of model parameters.

You can see the number of parameters (or degrees of freedom) that each input

contributes to the model, as well as each input's statistical significance, by

viewing lines 117-146 of the Output window.

The Type 3

Analysis tests the statistical significance of adding the indicated input to a

model that already contains other listed inputs. Roughly speaking, a value near

0 in the Pr > Chi-Square column indicates a significant input; a

value near 1 indicates an extraneous input.

Type 3 Analysis of Effects

Wald

Effect DF Chi-Square Pr > ChiSq

DemCluster

53 44.0996 0.8030

DemGender

2 0.0032 0.9984

DemHomeOwner 1 0.0213 0.8840

DemMedHomeValue

1 9.3921 0.0022

DemPctVeterans

1 0.1334 0.7150

GiftAvg36

1 4.5339 0.0332

GiftAvgAll

1 0.8113 0.3677

GiftAvgLast

1 0.0003 0.9874

GiftCnt36

1 0.6848 0.4079

GiftCntAll

1 0.0144 0.9044

GiftCntCard36

1 2.4447 0.1179

GiftCntCardAll

1 0.0073 0.9320

GiftTimeFirst

1 3.8204 0.0506

GiftTimeLast 1 15.8614 <.0001

IMP_DemAge

1 4.7087 0.0300

IMP_DemIncomeGroup 1 11.1804 0.0008

IMP_GiftAvgCard36 1 0.0758 0.7830

M_DemAge 1 0.3366 0.5618

M_DemIncomeGroup 1 0.0480 0.8266

M_GiftAvgCard36

1 5.4579 0.0195

PromCnt12

1 3.4896 0.0618

PromCnt36

1 4.8168 0.0282

PromCntAll

1 0.2440 0.6214

PromCntCard12

1 0.2867 0.5923

PromCntCard36

1 1.1416 0.2853

PromCntCardAll

1 1.6851 0.1942

StatusCat96NK

5 6.5422 0.2570

StatusCatStarAll 1 2.7676 0.0962

The

statistical significance measures range from <0.0001 (highly significant) to

0.9997 (highly dubious). Results such as this suggest that certain inputs can

be dropped without affecting the predictive prowess of the model.

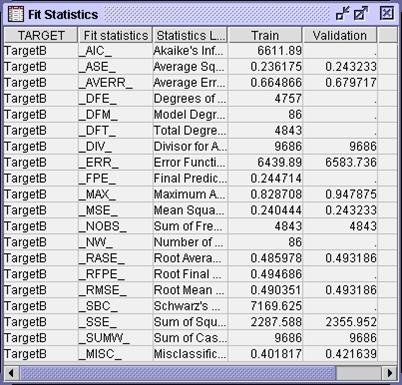

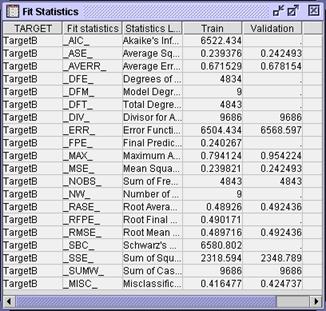

Restore the

Output window to its original size and maximize the Fit Statistics window.

If

the decision predictions are of interest, model fit can be judged by

misclassification. If estimate predictions are the focus, model fit can be

assessed by average square error. There appears to be some discrepancy between

the values of these two statistics on the train and validation data. This

indicates possible overfit of the model. It can be mitigated by employing an

input selection procedure.

The second task that all predictive models should

perform is input selection. One way to find the optimal set of inputs for a

regression is simply to try every combination. Unfortunately, the number of

models to consider using this approach increases exponentially in the number of

available inputs. Such an exhaustive search is impractical for realistic

prediction problems.

An alternative to the exhaustive search is to restrict the search to a

sequence of improving models. While this might not find the single best model,

it is commonly used to find models with good predictive performance. The

Regression node in SAS Enterprise Miner provides three sequential selection

methods.

Forward selection creates a

sequence of models of increasing complexity. The sequence starts with the

baseline model, a model predicting the overall average target value for all

cases. The algorithm searches the set of one-input models and selects the model

that most improves upon the baseline model. It then searches the set of

two-input models that contain the input selected in the previous step and

selects the model showing the most significant improvement. By adding a new

input to those selected in the previous step, a nested sequence of increasingly

complex models is generated. The sequence terminates when no significant

improvement can be made.

Improvement is quantified by the usual statistical measure of

significance, the p-value. Adding terms in this nested fashion always

increases a model's overall fit statistic. By calculating the change in the fit

statistic and assuming that the change conforms to a chi-squared distribution,

a significance probability, or p-value,

can be calculated. A large fit statistic change (corresponding to a large

chi-squared value) is unlikely due to chance. Therefore, a small p-value indicates a significant

improvement. When no p-value is below

a predetermined entry cutoff, the

forward selection procedure terminates.

In contrast to forward selection,

backward selection creates a sequence of models of decreasing complexity. The sequence starts with a saturated model, which

is a model that contains all available inputs and, therefore, has the highest

possible fit statistic. Inputs are sequentially removed from the model. At each

step, the input chosen for removal least reduces the overall model fit

statistic. This is equivalent to removing the input with the highest p-value. The sequence terminates when

all remaining inputs have a

p-value in excess of the

predetermined stay cutoff.

Stepwise selection combines elements from both the forward and backward selection

procedures. The method begins in the same way as the forward procedure,

sequentially adding inputs with the smallest p‑value below the entry cutoff. After each input is added,

however, the algorithm re-evaluates the statistical significance of all

included inputs. If the p-value of

any of the included input exceeds a stay cutoff, the input is removed from the

model and re-entered into the pool of inputs that are available for inclusion

in a subsequent step. The process terminates when all inputs available for

inclusion in the model have p-values

in excess of the entry cutoff and all inputs already included in the model have

p-values below the stay cutoff.

Selecting Inputs

Implementing a sequential

selection method in the regression node requires a minor change to the

Regression node settings.

Close the Regression results

window.

Select Selection Model Stepwise on the

Regression node property sheet.

The Regression node is now

configured to use stepwise selection to choose inputs for the model.

Run the Regression node and

view the results.

Select the Output tab and scroll to lines

95-121.

The stepwise procedure

starts with Step 0, an intercept-only regression model. The value of the

intercept parameter is chosen so that the model predicts the overall target

mean for every case. The parameter estimate and the training data target

measurements are combined in an objective function. The objective function is

determined by the model form and the error distribution of the target. The

value of the objective function for the intercept-only model is compared to the

values obtained in subsequent steps for more complex models. A large decrease

in the objective function for the more complex model indicates a significantly

better model.

Optimization Results

Iterations 0 Function Calls 3

Hessian Calls 1 Active Constraints 0

Objective Function 3356.9116922 Max Abs Gradient Element 7.225331E-12

Ridge 0 Actual Over Pred Change 0

Convergence criterion (ABSGCONV=0.00001) satisfied.

Likelihood Ratio Test

for Global Null Hypothesis: BETA=0

-2 Log

Likelihood Likelihood

Intercept Intercept & Ratio

Only Covariates Chi-Square DF Pr > ChiSq

6713.823 6713.823 0.0000 0 .

Analysis of Maximum

Likelihood Estimates

Standard Wald Standardized

Parameter DF Estimate Error Chi-Square Pr > ChiSq Estimate Exp(Est)

Intercept 1 -0.00041 0.0287 0.00 0.9885 1.000

Step 1 adds one input to the

intercept-only model. The input and corresponding parameter are chosen to

produce the largest decrease in the objective function. To estimate the values

of the model parameters, the modeling algorithm makes an initial guess for their

values. The initial guess is combined with the training data measurements in

the objective function. Based on statistical theory, the objective function is

assumed to take its minimum value at the correct estimate for the parameters. The

algorithm decides whether changing the values of the initial parameter

estimates can decrease the value of objective function. If so, the parameter

estimates are changed to decrease the value of the objective function and the

process iterates. The algorithm continues iterating until changes in the

parameter estimates fail to substantially decrease the value of the objective

function.

The Step 1 optimization is

summarized in the Output window, lines 121-164.

Step 1: Effect

GiftCntCard36 entered.

The DMREG Procedure

Newton-Raphson Ridge

Optimization

Without Parameter

Scaling

Parameter

Estimates 2

Optimization Start

Active Constraints 0 Objective Function 3356.9116922

Max Abs Gradient Element 118.98162296

Ratio

Between

Actual

Objective Max

Abs and

Function Active Objective Function Gradient Predicted

Iter Restarts Calls Constraints Function Change Element Ridge Change

1 0 2 0 3308 48.5172 2.3587 0 1.014

2 0 3 0 3308 0.0416 0.00805 0 1.002

3 0 4 0 3308 2.979E- 6.214E-8 0 1.000

Optimization Results

Iterations 3 Function Calls 6

Hessian Calls 4 Active Constraints 0

Objective Function 3308.3529331 Max Abs Gradient Element 6.2144229E-8

Ridge

0 Actual Over Pred Change 0.9999995175

Convergence criterion (GCONV=1E-6) satisfied.

The

output next compares the model fit in step 1 with the model fit in step 0. The

objective functions of both models are multiplied by 2 and differenced. The

difference is assumed to have a chi-square distribution with 1 degree of

freedom. The hypothesis that the two models are identical is tested. A large

value for the chi-square statistic makes this hypothesis unlikely.

The

hypothesis test is summarized in lines 167-173.

Likelihood Ratio Test for Global Null Hypothesis: BETA=0

-2 Log Likelihood Likelihood

Intercept Intercept & Ratio

Only Covariates Chi-Square DF Pr > ChiSq

6713.823 6616.706 97.1175 1 <.0001

Next, the output summarizes an analysis of the

statistical significance of individual model effects (lines 176-181). For the

one input model, this is similar to the global significance test above.

Type 3 Analysis of

Effects

Wald

Effect DF Chi-Square Pr > ChiSq

GiftCntCard36

1 93.0507 <.0001

Finally,

an analysis of individual parameter estimates is made. The standardized

estimates and the odds ratios merit special attention.

Analysis

of Maximum Likelihood Estimates

Standard Wald Standardized

Parameter DF Estimate Error Chi-Square Pr > ChiSq Estimate Exp(Est)

Intercept 1 -0.3360 0.0450 55.78 <.0001 0.715

GiftCntCard36 1 0.1841 0.0191 93.05 <.0001 0.1596 1.202

Odds

Ratio Estimates

Point

Effect Estimate

GiftCntCard36 1.202

The standardized estimates

present the effect of the input on the log-odds of donation. The values are

standardized to be independent of the input's unit of measure. This provides a

means of ranking the importance of inputs in the model.

The odds ratio estimates

indicate by what factor the odds of donation increase for each unit change in

the associated input. Combined with knowledge of the range of the input, this

provides an excellent way to judge the practical (as opposed to the

statistical) importance of an input in the model.

The stepwise selection

process continues for seven steps. After the eighth step, neither adding nor

removing inputs from the model significantly changes the model fit statistic. At

this point the Output window provides a summary of the stepwise procedure. The

summary shows the step in which each input was added and the statistical

significance of each input in the final eight-input model (lines 810-825).

NOTE: No (additional) effects met the 0.05 significance

level for entry into the model.

Summary of Stepwise Selection

Effect Number Score Wald

Step Entered DF In Chi-Square Chi-Square Pr > ChiSq

1 GiftCntCard36 1 1 95.6966 <.0001

2 GiftTimeLast 1 2 29.9410 <.0001

3 DemMedHomeValue 1 3 25.5086 <.0001

4 GiftTimeFirst 1 4 15.1942 <.0001

5 GiftAvg36 1 5 13.2369 0.0003

6 IMP_DemIncomeGroup 1 6 13.3458 0.0003

7 M_GiftAvgCard36 1 7 10.0412 0.0015

8 IMP_DemAge 1 8 4.2718 0.0387

The default

selection criterion selects the model from step 8 as the model with optimal

complexity (lines 828-830). As the next section shows, this might not be the

optimal based on the fit statistic that is appropriate for your analysis

objective.

The

selected model, based on the CHOOSE=NONE criterion, is the model trained in

Step 8. It consists of the following effects:

Intercept DemMedHomeValue GiftAvg36 GiftCntCard36 GiftTimeFirst GiftTimeLast IMP_DemAge IMP_DemIncomeGroup M_GiftAvgCard36

For convenience, the output

from step 9 is repeated. An excerpt from the analysis of individual parameter

estimates is shown below (lines 857-870).

Analysis

of Maximum Likelihood Estimates

Standard Wald Standardized

Parameter DF Estimate Error Chi-Square Pr > ChiSq Estimate Exp(Est)

Intercept 1 -0.3363 0.2223 2.29 0.1304 0.714

DemMedHomeValue 1 1.349E-6 3.177E-7 18.03 <.0001 0.0737 1.000

GiftAvg36 1 -0.0131 0.00344 14.59 0.0001 -0.0712 0.987

GiftCntCard36 1 0.1049 0.0242 18.80 <.0001 0.0910 1.111

GiftTimeFirst 1 0.00305 0.000807 14.28 0.0002 0.0631 1.003

GiftTimeLast 1 -0.0376 0.00747 25.32 <.0001 -0.0848 0.963

IMP_DemAge 1 0.00440 0.00213 4.27 0.0389 0.0347 1.004

IMP_DemIncomeGroup 1 0.0758 0.0192 15.55 <.0001 0.0680 1.079

M_GiftAvgCard36 0 1 0.1449 0.0462 9.83 0.0017 1.156

The parameter with the

largest standardized estimate is GiftCntCard36

The odds ratio estimates

show that a unit change in M_GiftAvgCard36 produces the largest change in the donation odds.

Point

Effect Estimate

DemMedHomeValue 1.000

GiftAvg36 0.987

GiftCntCard36 1.111

GiftTimeFirst

1.003

GiftTimeLast 0.963

IMP_DemAge 1.004

IMP_DemIncomeGroup 1.079

M_GiftAvgCard36 0 vs 1 1.336

Restore

the Output window and maximize the Fit Statistics window.

Considering the

analysis from an estimate prediction perspective, the simpler stepwise

selection model, with a lower validation average squared error, is an

improvement over the full model (from the previous section). From a decision

prediction perspective, however, the larger full model, with a slightly lower

misclassification, is preferred.

This somewhat

ambiguous result comes from a lack of complexity optimization, by default, in

the Regression node. This oversight is handled in the next demonstration.

Regression complexity

is optimized by choosing the optimal model in the sequential selection

sequence.

The process

involves two steps. First, fit statistics are calculated for the models

generated in each step of the selection process using both the training and

validation data sets.

Then, as with the

decision tree in Chapter 4, the simplest model (that is, the one with the

fewest inputs) with the optimal fit statistic is selected.

Optimizing Complexity

In the same

manner as the decision tree, you can tune a regression model to give optimal

performance on the validation data. The basic idea involves calculating a fit

statistic for each step in the input selection procedure and selecting the step

(and corresponding model) with the optimal fit statistic value. To avoid bias,

of course, the fit statistic should be calculated on the validation data set.

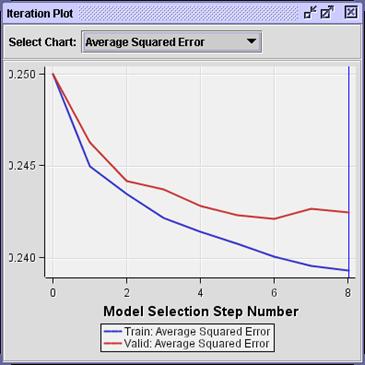

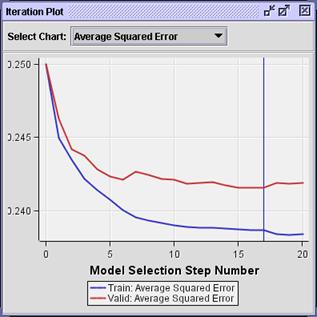

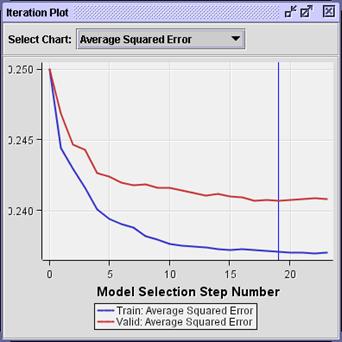

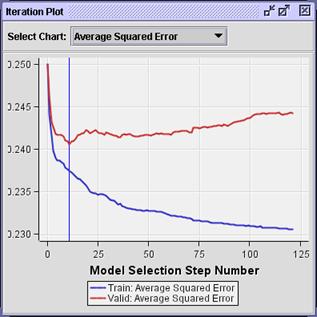

Select View Model

Iteration

Plot. The Iteration Plot window opens.

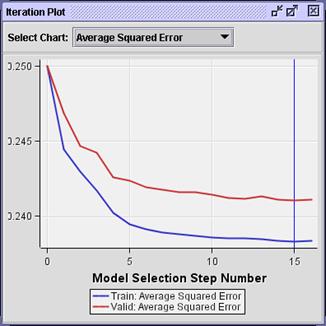

The

Iteration Plot window shows (by default) the average squared error from the

model selected in each step of the stepwise selection process. Apparently, the

smallest average squared error occurs in step 6, rather than in the final

model, step 8. If your analysis objective requires estimates predictions, the

model from step 6 should provide slightly less biased ones.

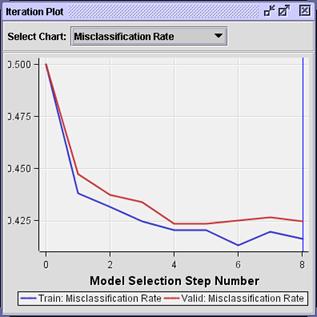

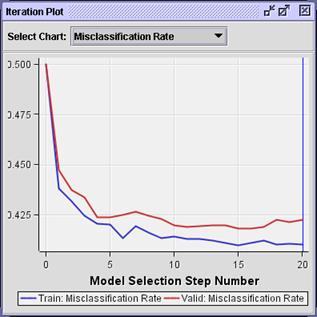

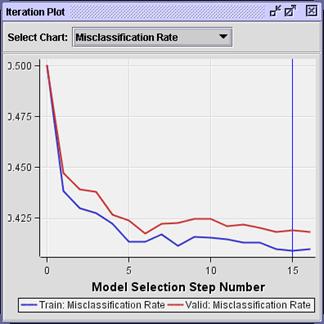

Select Select Chart

Misclassification Rate.

The

iteration plot shows that the model with the smallest misclassification rate

occurs in step 4. If your analysis objective requires decision predictions, the

predictions from the step 4 model will be as accurate as the predictions from

the final step 8 model.

The

selection process stopped at step 8 to limit the amount of time spent running

the stepwise selection procedure. In step 8, no more inputs had a chi-squared p-value below 0.05. The value 0.05 is a

somewhat arbitrary holdover from the days of statistical tables. With the

validation data available to gauge overfitting, it is possible to eliminate

this restriction and obtain a richer pool of models to consider.

Close the Results -

Regression window.

Select Use Selection Default

No from the Regression node Properties

panel.

Type in the Entry Significance

Level

field.

Type in the Stay Significance

Level

field.

The

Entry Significance value enables any input into the model. (The one chosen will

have the smallest p-value.) The Stay

Significance value keeps any input in the model with a p-value less than 0.5. This second choice is somewhat arbitrary. A

smaller value can terminate the stepwise selection process earlier, while a

larger value can maintain it longer. A Stay Significance of 1.0 forces stepwise

to behave in the manner of a forward selection.

Run the Regression node and

view the results.

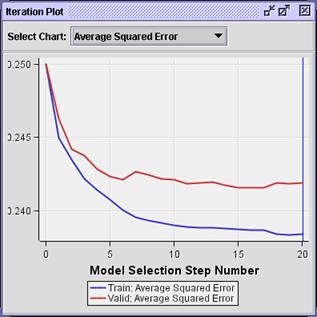

Select View

Model

Iteration

Plot. The Iteration Plot window opens.

The

iteration plot shows the smallest average squared errors occurring in steps 15

or 16.

Select Select Chart Misclassification

Rate.

The

iteration plot shows the smallest validation misclassification rates also

occurring near steps 15-16.

You

can configure the Regression node to select the model with the smallest fit

statistic (rather than the final stepwise selection iteration). This method is

how SAS Enterprise Miner optimizes complexity for regression models.

Close the Results -

Regression window.

If your predictions are decisions, use the following setting:

Select Selection

Criterion Validation

Misclassification. (Equivalently, you can select

Validation Profit / Loss. The

equivalence is demonstrated in Chapter 7.)

If your predictions are

estimates (or rankings), use the following setting:

Select Selection

Criterion Validation

Error.

The continuing

demonstration assumes validation error selection criteria.

Run the Regression node and

view the results.

Select View Model

Iteration

Plot.

The

vertical blue line shows the model with the optimal validation average squared

error (step 17).

Select the Output window and view lines 2256-2276.

Analysis of Maximum Likelihood

Estimates

Standard Wald Standardized

Parameter DF Estimate Error Chi-Square Pr > ChiSq Estimate Exp(Est)

Intercept 1 -0.3042 0.2892 1.11 0.2929 0.738

DemMedHomeValue 1 1.352E-6 3.183E-7 18.05 <.0001 0.0739 1.000

GiftAvg36 1 -0.0144 0.00506 8.14 0.0043 -0.0782 0.986

GiftAvgAll 1 0.00592 0.00543 1.19 0.2752 0.0326 1.006

GiftCnt36 1 0.0343 0.0305 1.27 0.2606 0.0397 1.035

GiftCntCard36 1 0.0737 0.0414 3.17 0.0751 0.0639 1.076

GiftTimeFirst 1 0.00440 0.00261 2.85 0.0914 0.0911 1.004

GiftTimeLast 1 -0.0410 0.00927 19.56 <.0001 -0.0925 0.960

IMP_DemAge 1 0.00452 0.00213 4.48 0.0344 0.0356 1.005

IMP_DemIncomeGroup 1 0.0784 0.0193 16.45 <.0001 0.0703 1.082

M_GiftAvgCard36 0 1 0.2776 0.0884 9.86 0.0017 1.320

PromCnt12 1 -0.0224 0.0132 2.90 0.0887 -0.0607 0.978

PromCnt36 1 0.0236 0.0116 4.13 0.0422 0.1005 1.024

PromCntCard36 1 -0.0362 0.0215 2.83 0.0925 -0.0909 0.964

PromCntCardAll 1 -0.0132 0.0140 0.88 0.3471 -0.0620 0.987

StatusCatStarAll 0 1 -0.0763 0.0392 3.79 0.0516 0.927

While not all the p-values are

less than 0.05, the model seems to have a better validation average square

error (and misclassification) than the model selected using the default

Significance Level settings.

In short, there is nothing sacred about 0.05. It is not unreasonable to

override the defaults of the Regression node to enable selection from a richer

collection of potential models. On the other hand, most of the reduction in the

fit statistics occurs during inclusion of the first 10 inputs. If you seek a

parsimonious model, it is reasonable to use a smaller value for the Stay Significance

parameter

Classical

regression analysis makes no assumptions about the distribution of inputs. The

only assumption is that the expected value of the target (or some function

thereof) is a linear combination of input measurements.

Why should you worry

about extreme input distributions?

There are at

least two compelling reasons.

First, in most real-world

applications, the relationship between expected target value and input value

does not increase without bound. Rather, it typically tapers off to some

horizontal asymptote. Standard regression models are unable to accommodate such

a relationship.

Second, as a point expands

from the overall mean of a distribution, the point has more influence, or leverage, on model fit. Models built on

inputs with extreme distributions attempt to optimize fit for the most extreme

points at the cost of fit for the bulk of the data, usually near the input

mean. This can result in an exaggeration or an understating of an input's

association with the target, or both.

The first

concern can be addressed by abandoning standard regression models for more

flexible modeling methods. Abandoning standard regression models is often done

at the cost of model interpretability and, more importantly, failure to address

the second concern: leverage.

A simpler and, arguably,

more effective approach is to transform offending inputs to less extreme forms

and build models on these transformed inputs, which not only reduces the

influence of extreme cases, but also creates an asymptotic association between

input and target on the original input scale.

Transforming Inputs

Regression models (such as clustering models) are sensitive to extreme or outlying values in the input space.

Inputs with highly skewed or highly kurtotic distributions can be selected over

inputs that yield better overall predictions. To avoid this problem, analysts

often regularize the input distributions using a simple transformation.

The benefit of this approach is improved model performance. The cost, of

course, is increased difficulty in model interpretation.

The Transform Variables tool enables you to easily apply standard

transformations (in addition to the specialized ones seen in Chapter 3) to a

set of inputs.

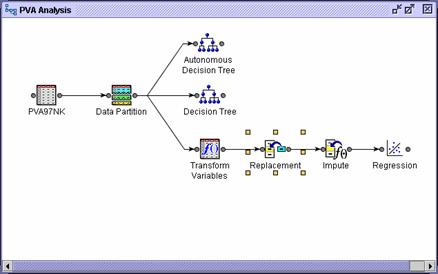

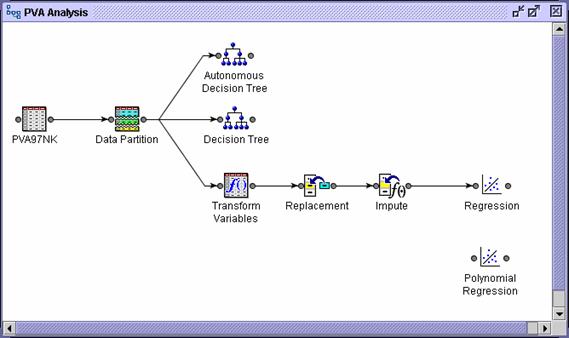

Remove the connection between the Data Partition node and the Impute node.

Select the Modify tab.

Drag a Transform Variables

tool into the diagram workspace.

Connect the Data Partition node to the Transform Variables node.

Connect the Transform Variables node to the Impute node.

Adjust the diagram icons for aesthetics.

The Transform Variables node is placed before the

Impute node to keep the imputed values at the average (or center of mass) of

the model inputs.

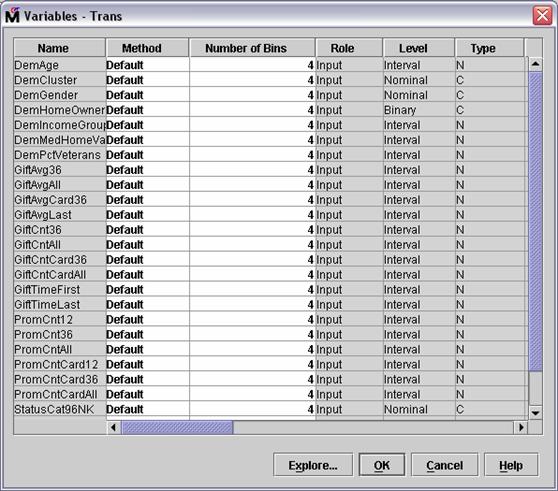

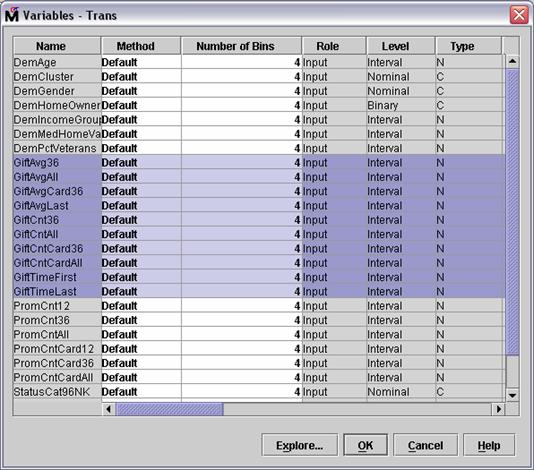

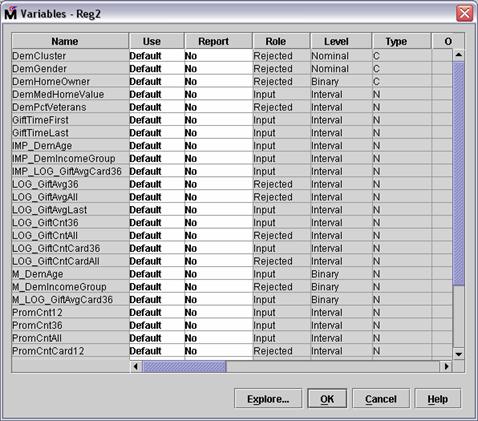

Select the Variables .

property of the Transform Variables node.

The Variables

- Trans window opens.

Select all inputs with Gift in the

name.

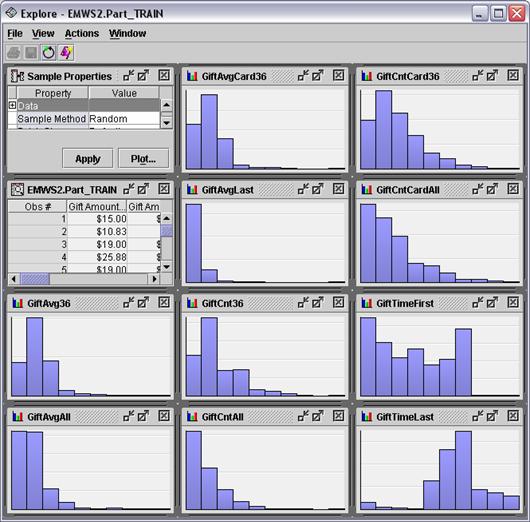

Select Explore . . The Explore

window opens.

The GiftAvg and GiftCnt inputs show some degree of skewness in their

distribution. The GiftTime inputs do not. To regularize the skewed distributions,

use the log transformation. For these inputs, the order of magnitude of the

underlying measure will predict the target rather than the measure itself.

Close the Explore window.

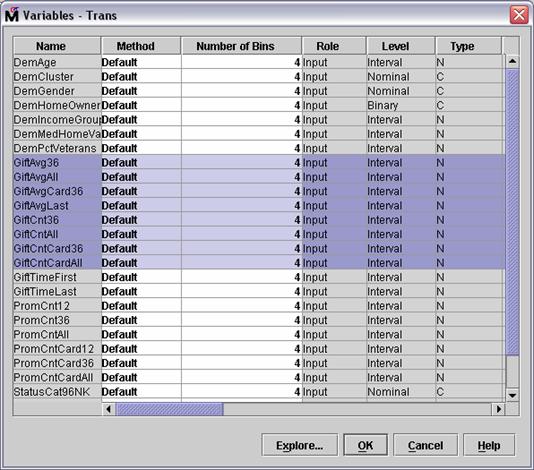

Deselect the two inputs with GiftTime in their names.

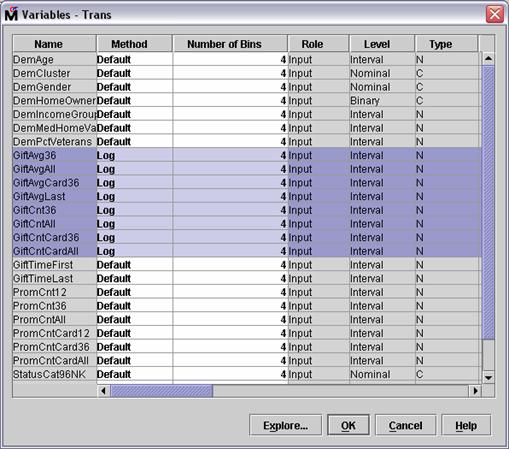

Select Method Log for one of the remaining

selected inputs. The selected method changes from Default to Log for

the GiftAvg and GiftCnt

inputs.

Select OK to close the Variables

- Trans window.

Run the Transform Variables node and view the results.

Maximize the Output window and examine lines 20-30.

Input Output

Input Name Role Level Output Name Level Formula

GiftAvg36 INPUT INTERVAL LOG_GiftAvg36 INTERVAL log(GiftAvg36 + 1)

GiftAvgAll INPUT INTERVAL LOG_GiftAvgAll INTERVAL log(GiftAvgAll + 1)

GiftAvgCard36 INPUT INTERVAL LOG_GiftAvgCard36 INTERVAL log(GiftAvgCard36 + 1)

GiftAvgLast INPUT INTERVAL LOG_GiftAvgLast INTERVAL log(GiftAvgLast + 1)

GiftCnt36 INPUT INTERVAL LOG_GiftCnt36 INTERVAL log(GiftCnt36 + 1)

GiftCntAll INPUT INTERVAL LOG_GiftCntAll INTERVAL log(GiftCntAll + 1)

GiftCntCard36 INPUT INTERVAL LOG_GiftCntCard36 INTERVAL log(GiftCntCard36 + 1)

GiftCntCardAll INPUT INTERVAL LOG_GiftCntCardAll INTERVAL log(GiftCntCardAll + 1)

Notice the Formula

column. While a log transformation was specified, the

actual transformation used was log(input

+ 1). This default action of the Transform Variables tool avoids problems with

0-values of the underlying inputs.

Close the Transform Variables - Results window.

Run the diagram from the Regression node and view the results.

Examine lines 1653 to 1680 the Output window.

Summary of Stepwise Selection

Effect Number Score Wald

Step Entered Removed DF In Chi-Square Chi-Square Pr > ChiSq

1 LOG_GiftCntCard36 1 1 107.6034 <.0001

2 GiftTimeLast 1 2 29.0312 <.0001

3 DemMedHomeValue 1 3 24.8434 <.0001

4 LOG_GiftAvgAll 1 4 28.9692 <.0001

5 IMP_DemIncomeGroup 1 5 13.8240 0.0002

6 GiftTimeFirst 1 6 7.1299 0.0076

7 IMP_DemAge 1 7 4.1407 0.0419

8 LOG_GiftAvgLast 1 8 2.6302 0.1048

9 PromCntCard12 1 9 1.8469 0.1741

10 StatusCatStarAll 1 10 1.8604 0.1726

11 IMP_LOG_GiftAvgCard36 1 11 1.4821 0.2234

LOG_GiftAvgAll 1 10 0.4217 0.5161

13 M_LOG_GiftAvgCard36 1 11 2.0584 0.1514

14 LOG_GiftCnt36 1 12 1.8949 0.1687

15 DemPctVeterans 1 13 0.3578 0.5498

16 DemPctVeterans 1 12 0.3577 0.5498

The selected model, based on the CHOOSE=VERROR criterion,

is the model trained in Step 15. It consists of the following effects:

Intercept DemMedHomeValue DemPctVeterans GiftTimeFirst GiftTimeLast IMP_DemAge IMP_DemIncomeGroup IMP_LOG_GiftAvgCard36 LOG_GiftAvgLast LOG_GiftCnt36 LOG_GiftCntCard36 M_LOG_GiftAvgCard36 PromCntCard12 StatusCatStarAll

The stepwise selection process took 16 steps, and

the selected model came from step 15. Notice that many of the inputs selected

are log transformations of the original.

Lines 1710 to 1750 show more statistics from the selected model.

Analysis of Maximum Likelihood

Estimates

Standard Wald Standardized

Parameter DF Estimate Error Chi-Square Pr > ChiSq Estimate Exp(Est)

Intercept 1 0.2908 0.3490 0.69 0.4047 1.338

DemMedHomeValue 1 1.381E-6 3.173E-7 18.94 <.0001 0.0754 1.000

DemPctVeterans 1 0.00155 0.00260 0.36 0.5498 0.00977 1.002

GiftTimeFirst 1 0.00210 0.000958 4.82 0.0281 0.0436 1.002

GiftTimeLast 1 -0.0369 0.00810 20.70 <.0001 -0.0831 0.964

IMP_DemAge 1 0.00419 0.00214 3.85 0.0498 0.0330 1.004

IMP_DemIncomeGroup 1 0.0821 0.0193 18.03 <.0001 0.0737 1.086

IMP_LOG_GiftAvgCard36 1 -0.1880 0.0985 3.65 0.0562 -0.0479 0.829

LOG_GiftAvgLast 1 -0.1101 0.0828 1.77 0.1837 -0.0334 0.896

LOG_GiftCnt36 1 0.1579 0.1165 1.84 0.1752 0.0417 1.171

LOG_GiftCntCard36 1 0.1983 0.1269 2.44 0.1183 0.0610 1.219

M_LOG_GiftAvgCard36 0 1 0.1111 0.0657 2.86 0.0910 1.117

PromCntCard12 1 -0.0418 0.0259 2.60 0.1069 -0.0305 0.959

StatusCatStarAll 0 1 -0.0529 0.0388 1.86 0.1729 0.948

Odds Ratio Estimates

Point

Effect Estimate

DemMedHomeValue 1.000

DemPctVeterans 1.002

GiftTimeFirst 1.002

GiftTimeLast 0.964

IMP_DemAge 1.004

IMP_DemIncomeGroup 1.086

IMP_LOG_GiftAvgCard36 0.829

LOG_GiftAvgLast 0.896

LOG_GiftCnt36 1.171

LOG_GiftCntCard36 1.219

M_LOG_GiftAvgCard36 0 vs 1 1.249

PromCntCard12 0.959

StatusCatStarAll 0 vs 1 0.900

Select View Model Iteration Plot.

Again, the selected model (based on minimum

average squared error) occurs in step 15. The actual value of average squared

error for this model is slightly lower than that for the model with the

untransformed inputs.

Select Select Chart Misclassification Rate.

The misclassification rate with the transformed

input is also lower than that for the untransformed inputs. However, the model

with the lowest misclassification rate comes from step 6. If you want to

optimize on misclassification rate, you must change this property in the

Regression node's property sheet.

Categorical inputs present

another problem for regressions. To represent these non-numeric inputs in a

model, you must convert them to some sort of numeric values. This conversion is

most commonly done by creating design variables (or dummy variables), with each design variable representing, roughly,

one level of the categorical input. (The total number of design variables

required is, in fact, one less than the number of inputs.) A single categorical

input can vastly increase a model's degrees of freedom, which, in turn,

increases the chances of a model overfitting.

There are many remedies to this problem. One of

the simplest remedies is to use domain knowledge to reduce the number of levels

of the categorical input.

Recoding Categorical Inputs

The demonstration shows how to use the Replacement tool to facilitate

combining input levels.

Remove the connection between the Transform Variables

node and the Impute node.

Select the Modify tab.

Drag a Replacement tool into the diagram workspace.

Connect the Transform Variables node to the Replacement node.

Connect the Replacement node to the Impute node.

Select Replacement Editor .

from the Replacement node Properties panel. A confirmation dialog box opens.

Select Yes. The Replacement

Editor opens.

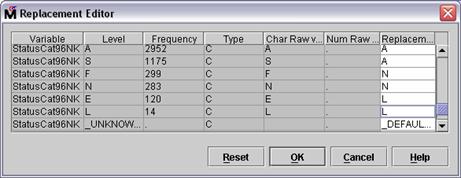

The Replacement Editor lists

all levels of all categorical inputs. You can use the Replacement column to

reassign values to any of the levels.

The input with the largest

number of levels is DemCluster, which has so many levels that consolidating the levels using the

Replacement Editor would be an arduous task. (Another, autonomous method for

consolidating the levels of DemCluster (or any categorical input) is presented as a special topic in Chapter

9.)

For this demonstration,

combine the levels of another input, StatusCat96NK

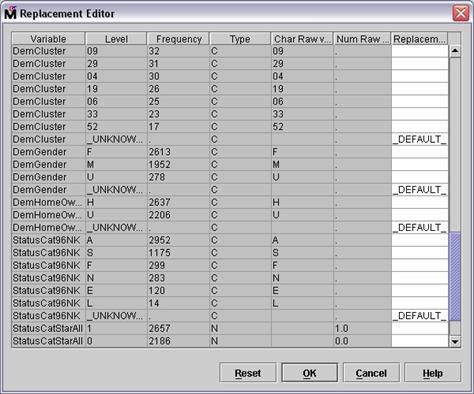

Scroll the Replacement Editor to view the levels of StatusCat96NK

The input has six levels,

plus a level to represent unknown values (which do not occur in the training

data). The levels of StatusCat96NK will be consolidated as follows:

Levels A and S (active and star donors) indicate consistent donors and are

grouped into a single level, A.

Levels F and N (first-time and new donors) indicate new donors and are

grouped into a single level, N.

Levels E and L (inactive and lapsing donors) indicate lapsing donors

and are grouped into a single level L.

Type A in the Replacement field for StatusCat96NK levels A and S.

Type N in the Replacement field for StatusCat96NK levels F and N.

Type L in the Replacement field for StatusCat96NK levels L and E.

Select OK to close

the Replacement Editor.

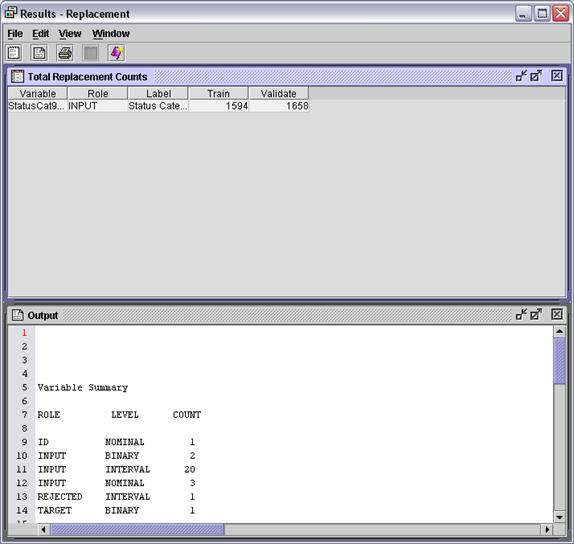

Run the Replacement node and view the results.

The Total Replacement Counts

window shows the number of replacements that occurr in the training and

validation data.

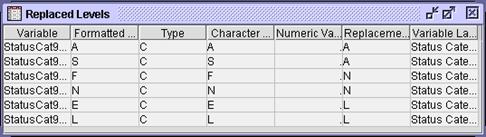

Select View Model Replaced Levels. The

Replaced Levels window opens.

The replaced level values are

consistent with expectations.

Close the Results window.

Run the Regression node and view the results.

View lines 2310-2340 of the

Output window.

Summary

of Stepwise Selection

Effect Number Score Wald

Step Entered Removed DF In Chi-Square Chi-Square Pr > ChiSq

1 LOG_GiftCntCard36 1 1 107.6034 <.0001

2 GiftTimeLast 1 2 29.0312 <.0001

3 DemMedHomeValue 1 3 24.8434 <.0001

4 LOG_GiftAvgAll 1 4 28.9692 <.0001

5 IMP_DemIncomeGroup 1 5 13.8240 0.0002

6 GiftTimeFirst 1 6 7.1299 0.0076

7 IMP_DemAge 1 7 4.1407 0.0419

8 REPL_StatusCat96NK 2 8 5.2197 0.0735

9 IMP_LOG_GiftAvgCard36 1 9 2.4956 0.1142

10 M_LOG_GiftAvgCard36 1 10 1.6207 0.2030

11 StatusCatStarAll 1 11 1.9076 0.1672

12 LOG_GiftCnt36 1 12 1.5708 0.2101

13 LOG_GiftAvgLast 1 13 1.4316 0.2315

14 LOG_GiftAvgAll 1 12 0.2082 0.6482

15 PromCntCardAll 1 13 0.6704 0.4129

16 PromCnt36 1 14 1.0417 0.3074

17 PromCnt12 1 15 0.9800 0.3222

18 PromCntAll 1 16 1.0446 0.3068

19 M_DemAge 1 17 0.4815 0.4877

20 LOG_GiftCntAll 1 18 0.3887 0.5330

21 LOG_GiftCntAll 1 17 0.3886 0.5330

The REPL_StatusCat96NK input (created from the original StatusCat96NK input) is included in the stepwise selection process. The three-level

input is represented by two degrees of freedom.

View lines 2422-2423 of the Output window.

REPL_StatusCat96NK A vs N 0.822

REPL_StatusCat96NK L vs N 1.273

Based

on the odds ratios, active donors in the 96NK campaign are less likely than new

donors to contribute in the 97NK campaign. On the other hand, lapsing donors in

the 96NK campaign are more likely than new donors to contribute in the 97NK

campaign.

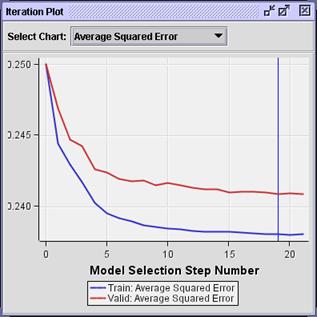

Select View

Model

Iteration

Plot.

The

selected model from step 19 has, again, a slightly smaller average squared

error than previous models.

The Regression tool assumes (by

default) a linear and additive association between the inputs and the logit of

the target. If the true association is more complicated, such an assumption might

result in biased predictions. For decisions and rankings, this bias can (in

some cases) be unimportant. For estimates, this bias will appear as a higher

value for the validation average squared error fit statistic.

In the dot color problem, the (standard logistic regression) assumption

that the concentration of yellow dots increases toward the upper-right corner

of the unit square seems to be suspect.

When minimizing prediction bias is important, you can increase the

flexibility of a regression model by adding polynomial combinations of the

model inputs. This enables predictions to better match the true input/target

association. It also increases the chances of overfitting while simultaneously

reducing the interpretability of the predictions. Therefore, polynomial

regression must be approached with some care.

In SAS Enterprise Miner, adding polynomial terms can be done selectively

or autonomously.

Adding Polynomial Regression Terms Selectively

This demonstration shows how to selectively add polynomial regression

terms.

You can modify the existing Regression node or add a new Regression node. If

you add a new node, you must configure the Polynomial Regression node to

perform the same tasks as the original. An alternative is to make a copy of the

existing node.

Right-click the Regression node

and select Copy from the

menu.

Right-click the diagram workspace and select Paste from the menu. A new Regression node is added with the

label Regression (2) to

distinguish it from the existing one.

Select the Regression (2)

node. The properties are identical to the existing node.

Rename the new regression node Polynomial Regression

Connect the Polynomial Regression node to the Impute node.

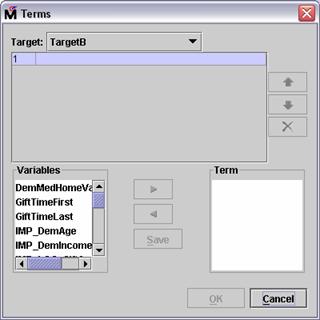

The Term Editor enables you to add specific polynomial

terms to the regression model.

Select Term Editor . from

the Polynomial Regression Properties panel. The Terms dialog box opens.

Suppose that you suspect an interaction between

home value and time since last gift. (Perhaps a recent change in property

values affected the donation patterns.)

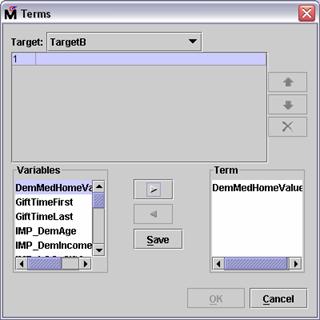

Select DemMedHomeValue in the

Variables panel of the Terms dialog box.

Select the Add button,  . The DemMedHomeValue input

is added to the Term panel.

. The DemMedHomeValue input

is added to the Term panel.

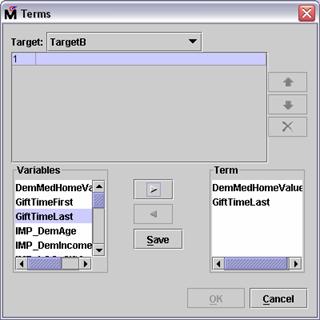

Repeat for GiftTimeLast

Select Save. An

interaction between the selected inputs is now available for consideration by

the regression node.

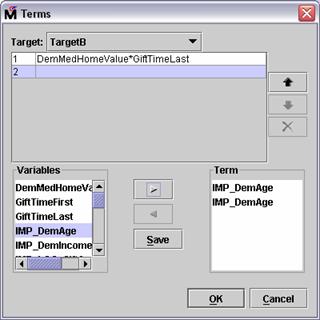

Similarly, suppose that you suspect a parabola-shaped

relationship between donation and donor age. (Donation odds increase with age,

peak, and then decline with age.)

Select IMP_DemAge

Select the Add button,  . The IMP_DemAge input

is added to the Term panel.

. The IMP_DemAge input

is added to the Term panel.

Select the Add button, again.

Another IMP_DemAge input

is added to the Term panel.

Select Save. A quadratic

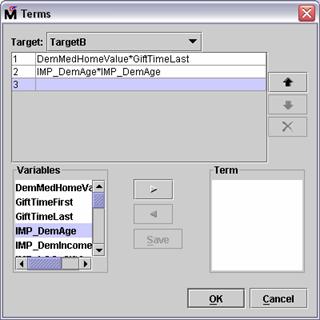

age term is available for consideration by the model.

Select OK to close the Terms

dialog box.

To use the terms you defined in the Terms dialog

box, you must enable the User Terms option in the Regression node.

Select User Terms Yes in the Polynomial Regression

Properties panel.

Run the Polynomial Regression node and view the results.

Scroll the Output window to lines 2515-2540.

Summary of Stepwise Selection

Effect Number Score Wald

Step Entered Removed DF In Chi-Square Chi-Square Pr > ChiSq

1 LOG_GiftCntCard36 1 1 107.6034 <.0001

2 GiftTimeLast 1 2 29.0312 <.0001

3 DemMedHomeValue*GiftTimeLast 1 3 26.3762 <.0001

4 LOG_GiftAvgAll 1 4 29.2016 <.0001

5 IMP_DemIncomeGroup 1 5 13.8523 0.0002

6 GiftTimeFirst 1 6 7.1518 0.0075

7 IMP_DemAge 1 7 4.0914 0.0431

8 IMP_DemAge*IMP_DemAge 1 8 12.2214 0.0005

9 M_DemAge 1 9 4.1796 0.0409

10 REPL_StatusCat96NK 2 10 5.7905 0.0553

11 LOG_GiftAvgLast 1 11 2.3447 0.1257

12 StatusCatStarAll 1 12 1.8360 0.1754

13 LOG_GiftCnt36 1 13 1.3030 0.2537

14 M_LOG_GiftAvgCard36 1 14 1.6761 0.1954

15 IMP_LOG_GiftAvgCard36 1 15 1.7173 0.1900

16 LOG_GiftAvgAll 1 14 0.3704 0.5428

17 PromCntCardAll 1 15 1.0003 0.3172

18 PromCntAll 1 16 1.2101 0.2713

19 PromCnt12 1 17 0.6678 0.4138

20 PromCnt36 1 18 1.3816 0.2398

21 LOG_GiftCntAll 1 19 0.4570 0.4990

22 LOG_GiftAvgAll 1 20 0.3898 0.5324

23 LOG_GiftAvgAll 1 19 0.3897 0.5325

The stepwise selection summary shows the

polynomial terms added in steps 3 and 8.

View the Iteration Plot window.

While present in the selected model, the

interaction terms appear to have negligible effect on the model performance (at

least for average squared error).

This begs the question: How do you know which

non-linear terms to include in a model?

Unfortunately, there is no simple solution to this

question in SAS Enterprise Miner, short of trying all of them

Adding Polynomial Regression Terms

Autonomously

(Self-Study)

SAS Enterprise Miner has the ability to add every polynomial combination of inputs to a regression model.

Obviously, this feature must be used with some care, because the number of

polynomial input combinations increases rapidly with input count.

For instance, the PVA97NK data

set has 20 interval inputs. If you want to consider every quadratic combination

of these 20 inputs, your selection procedure must sequentially slog through

more than 200 inputs. This is not an overwhelming task for today's fast

computers, but there is a shortcut that many analysts use to reduce this count.

The trick is to only consider polynomial expressions of those inputs found

to be linearly related to the logit of the target. That is, start with those

inputs selected by the original regression model. A simple modification to your

analysis diagram makes this possible.

Delete the connection between the Impute

node and the Polynomial Regression

node.

Connect the Regression node to the Polynomial Regression node.

Right-click the Polynomial Regression node

and select Update from the menu.

A Status dialog box informs you of the completion of the update process.

Select OK to close the Status

dialog box.

Select Variables . from

the Polynomial Regression Properties panel.

All inputs not selected in the original regression's

stepwise procedure are rejected.

Select OK to close the Variables

dialog box.

Select Polynomial Terms Yes in the Polynomial Regression

Properties panel. This adds all quadratic combinations of the interval inputs.

You can increase this to a higher order polynomial by

changing the Polynomial Degree field.

Select User Terms No. The terms added in the last

demonstration will be included by specifying the Polynomial Terms option.

Run the Polynomial Regression node and view the results. (This might take

a few minutes to complete on slower computers.)

Scroll to the bottom of the Output window.

NOTE: File view has been

truncated.

Refer to C:Documents and

SettingsusernameMy DocumentsMy SAS Files9.1EM_ProjectsMy

ProjectWorkspacesEMWS2Reg2EMOUTPUT.out

on this server for entire

file contents.

The amount of output generated by the selection history exceeds the 10,000-line,

client-transfer limit of SAS Enterprise Miner. To view the complete output

listing, you must open the referenced file.

Doing so reveals a 121-step and 18,000-line input

selection free-for-all. The selection summary is shown below.

Summary of Stepwise Selection

Effect Number Score Wald

Step Entered Removed DF In Chi-Square Chi-Square Pr > ChiSq

1 IMP_DemAge*LOG_GiftCntCard36 1 1 112.3900 <.0001

2 GiftTimeLast*LOG_GiftAvgLast 1 2 50.4645 <.0001

3 DemMedHomeValue*IMP_DemIncomeGroup 1 3 35.6614 <.0001

4 GiftTimeFirst*IMP_DemIncomeGroup 1 4 15.9535 <.0001

5 DemMedHomeValue*GiftTimeLast 1 5 5.1609 0.0231

6 DemMedHomeValue*IMP_DemIncomeGroup 1 4 0.0257 0.8726

7 IMP_DemAge*PromCntCardAll 1 5 4.5051 0.0338

8 GiftTimeFirst*LOG_GiftCnt36 1 6 4.6421 0.0312

9 GiftTimeLast*LOG_GiftCntCard36 1 7 8.0742 0.0045

10 GiftTimeLast*IMP_DemIncomeGroup 1 8 3.7680 0.0522

11 StatusCatStarAll 1 9 4.0508 0.0442

12 M_LOG_GiftAvgCard36 1 10 4.9476 0.0261

13 IMP_DemIncomeGroup*IMP_DemIncomeGroup 1 11 3.3268 0.0682

14 IMP_DemIncomeGroup*LOG_GiftAvgLast 1 12 5.6563 0.0174

15 GiftTimeLast 1 13 6.6747 0.0098

16 GiftTimeLast*IMP_DemIncomeGroup 1 12 0.0375 0.8465

17 LOG_GiftCntCard36 1 13 5.4244 0.0199

18 IMP_DemAge*LOG_GiftAvgLast 1 14 5.0260 0.0250

19 IMP_DemAge*IMP_DemAge 1 15 5.7455 0.0165

20 IMP_DemAge 1 16 5.2865 0.0215

21 M_DemAge 1 17 8.9336 0.0028

22 LOG_GiftAvgLast*PromCntAll 1 18 2.6281 0.1050

23 LOG_GiftCnt36*LOG_GiftCnt36 1 19 2.5730 0.1087

24 GiftTimeFirst*IMP_DemIncomeGroup 1 18 0.0289 0.8651

25 GiftTimeFirst*PromCntAll 1 19 3.6941 0.0546

26 IMP_DemAge*LOG_GiftAvgLast 1 18 0.3456 0.5566

27 IMP_DemAge*LOG_GiftCntCard36 1 17 0.2592 0.6107

28 GiftTimeLast*PromCntAll 1 18 2.3912 0.1220

29 GiftTimeFirst*IMP_DemAge 1 19 1.9879 0.1586

30 LOG_GiftCnt36*PromCntCardAll 1 20 4.8338 0.0279

31 REPL_StatusCat96NK 2 21 3.4798 0.1755

32 IMP_DemAge*IMP_DemIncomeGroup 1 22 1.1337 0.2870

33 IMP_DemAge*IMP_LOG_GiftAvgCard36 1 23 1.0241 0.3116

34 GiftTimeLast*IMP_LOG_GiftAvgCard36 1 24 3.8889 0.0486

35 IMP_LOG_GiftAvgCard36 1 25 3.6415 0.0564

36 IMP_DemAge*IMP_LOG_GiftAvgCard36 1 24 0.2008 0.6541

37 IMP_LOG_GiftAvgCard36*LOG_GiftAvgLast 1 25 5.6166 0.0178

38 IMP_LOG_GiftAvgCard36*LOG_GiftCntCard36 1 26 2.8395 0.0920

39 LOG_GiftAvgLast 1 27 1.4026 0.2363

40 LOG_GiftAvgLast*LOG_GiftCntCard36 1 28 1.0598 0.3033

41 M_LOG_GiftAvgCard36 1 27 0.2257 0.6348

42 GiftTimeLast*PromCnt12 1 28 0.9554 0.3284

43 IMP_LOG_GiftAvgCard36*PromCnt36 1 29 1.1580 0.2819

44 GiftTimeFirst*PromCnt36 1 30 1.2396 0.2655

45 GiftTimeFirst*PromCntAll 1 29 0.0060 0.9380

(Continued on the next page.)

46 IMP_LOG_GiftAvgCard36*LOG_GiftCntCard36 1 28 0.4424 0.5060

47 IMP_LOG_GiftAvgCard36*IMP_LOG_GiftAvgCard36 1 29 1.0828 0.2981

48 LOG_GiftCnt36*PromCntAll 1 30 1.0412 0.3075

49 IMP_DemAge*PromCntCardAll 1 29 0.3676 0.5443

50 LOG_GiftAvgLast*PromCntCardAll 1 30 2.0774 0.1495

51 LOG_GiftCnt36*PromCntCardAll 1 29 0.3967 0.5288

52 PromCnt36*PromCntCardAll 1 30 1.2143 0.2705

53 GiftTimeLast*PromCntAll 1 29 0.4198 0.5170

54 LOG_GiftAvgLast*PromCnt36 1 30 0.9148 0.3388

55 PromCntAll 1 31 1.0177 0.3131

56 IMP_DemIncomeGroup*LOG_GiftCntCard36 1 32 0.8736 0.3500

57 IMP_DemIncomeGroup*LOG_GiftCnt36 1 33 1.3926 0.2380

58 GiftTimeLast*LOG_GiftCnt36 1 34 1.9062 0.1674

59 DemMedHomeValue*GiftTimeFirst 1 35 0.8606 0.3536

60 DemMedHomeValue*PromCnt12 1 36 1.7609 0.1845

61 DemMedHomeValue*DemMedHomeValue 1 37 1.6746 0.1956

62 IMP_LOG_GiftAvgCard36*PromCnt12 1 38 1.0289 0.3104

63 LOG_GiftAvgLast*PromCnt12 1 39 1.1348 0.2867

64 LOG_GiftCnt36*PromCnt12 1 40 0.8804 0.3481

65 PromCntAll 1 39 0.1284 0.7201

66 IMP_DemAge*PromCntAll 1 40 0.9530 0.3290

67 IMP_DemAge*PromCnt36 1 41 0.7239 0.3949

68 IMP_LOG_GiftAvgCard36*PromCntAll 1 42 0.7922 0.3734

69 GiftTimeFirst*IMP_LOG_GiftAvgCard36 1 43 1.1685 0.2797

70 IMP_DemIncomeGroup*PromCnt36 1 44 0.8058 0.3694

71 IMP_DemIncomeGroup*PromCntCardAll 1 45 1.7767 0.1826

72 IMP_DemIncomeGroup*PromCnt12 1 46 3.3905 0.0656

73 LOG_GiftAvgLast*PromCnt12 1 45 0.1157 0.7337

74 IMP_DemAge*IMP_DemIncomeGroup 1 44 0.3121 0.5764

75 IMP_DemIncomeGroup*PromCntAll 1 45 1.5760 0.2093

76 DemMedHomeValue*IMP_DemAge 1 46 0.7067 0.4005

77 DemMedHomeValue 1 47 0.8369 0.3603

78 GiftTimeLast*PromCntCardAll 1 48 0.6305 0.4272

79 GiftTimeLast*PromCnt36 1 49 1.3586 0.2438

80 IMP_DemAge*IMP_LOG_GiftAvgCard36 1 50 0.5447 0.4605

81 IMP_DemAge*LOG_GiftAvgLast 1 51 1.8152 0.1779

82 IMP_LOG_GiftAvgCard36*PromCntCardAll 1 52 0.5547 0.4564

83 PromCnt12*PromCnt12 1 53 0.4997 0.4796

84 PromCnt36*PromCntCardAll 1 52 0.2620 0.6088

85 GiftTimeFirst*IMP_LOG_GiftAvgCard36 1 51 0.3309 0.5651

86 GiftTimeFirst*GiftTimeLast 1 52 0.9405 0.3322

87 PromCnt12 1 53 0.6663 0.4143

88 PromCnt36 1 54 1.1938 0.2746

89 IMP_LOG_GiftAvgCard36*PromCnt12 1 53 0.1271 0.7215

90 LOG_GiftCnt36*LOG_GiftCntCard36 1 54 0.9120 0.3396

91 LOG_GiftCntCard36 1 53 0.1168 0.7326

92 LOG_GiftCntCard36*LOG_GiftCntCard36 1 54 1.2887 0.2563

93 LOG_GiftCntCard36*PromCnt36 1 55 0.8773 0.3489

94 PromCntCardAll 1 56 0.9834 0.3214

95 GiftTimeLast*PromCnt36 1 55 0.3743 0.5407

96 GiftTimeLast*PromCnt12 1 54 0.0612 0.8046

97 PromCnt36*PromCnt36 1 55 1.0367 0.3086

98 LOG_GiftAvgLast*LOG_GiftCnt36 1 56 0.7673 0.3811

99 GiftTimeLast*LOG_GiftCnt36 1 55 0.3944 0.5300

100 LOG_GiftCntCard36*PromCntCardAll 1 56 0.8257 0.3635

(Continued on the next page.)

101 LOG_GiftCntCard36*PromCntAll 1 57 2.3132 0.1283

102 GiftTimeFirst*PromCnt36 1 56 0.3471 0.5558

103 GiftTimeFirst*LOG_GiftCntCard36 1 57 1.6283 0.2019

104 LOG_GiftCntCard36*PromCnt36 1 56 0.0007 0.9792

105 LOG_GiftCnt36*PromCntAll 1 55 0.2986 0.5848

106 LOG_GiftCntCard36*PromCnt12 1 56 2.1837 0.1395

107 LOG_GiftCnt36*PromCnt12 1 55 0.1815 0.6701

108 GiftTimeLast 1 54 0.4189 0.5175

109 LOG_GiftCntCard36*PromCnt36 1 55 0.9461 0.3307

110 DemMedHomeValue*PromCnt36 1 56 0.5590 0.4547

111 DemMedHomeValue*PromCnt12 1 55 0.4496 0.5025

112 DemMedHomeValue*PromCntCardAll 1 56 0.8854 0.3467

DemMedHomeValue*GiftTimeFirst 1 55 0.0000 0.9972

114 GiftTimeLast*IMP_DemIncomeGroup 1 56 0.6227 0.4300

115 PromCnt12*PromCntAll 1 57 0.5536 0.4568

116 PromCnt12*PromCntCardAll 1 58 0.5737 0.4488

117 GiftTimeFirst 1 59 0.4895 0.4842

118 GiftTimeFirst*GiftTimeLast 1 58 0.1034 0.7478

119 GiftTimeFirst*LOG_GiftAvgLast 1 59 1.4562 0.2275

120 GiftTimeLast 1 60 0.3704 0.5428

121 GiftTimeLast 1 59 0.3701 0.5430

Examine the iteration plot.

Surprisingly, the selected model comes from step 12 and involves only a

few regression terms.

Analysis of Maximum Likelihood Estimates

Standard Wald Standardized

Parameter DF Estimate Error Chi-Square Pr > ChiSq Estimate Exp(Est)

Intercept 1 0.0164 0.1395 0.01 0.9063 1.017

StatusCatStarAll 0 1 -0.0761 0.0378 4.05 0.0442 0.927

DemMedHomeValue*GiftTimeLast 1 7.885E-8 1.694E-8 21.67 <.0001 1.000

GiftTimeFirst*IMP_DemIncomeGroup 1 0.000345 0.000324 1.13 0.2872 1.000

GiftTimeFirst*LOG_GiftCnt36 1 0.00309 0.000920 11.26 0.0008 1.003

GiftTimeLast*IMP_DemIncomeGroup 1 0.00327 0.00157 4.34 0.0371 1.003

GiftTimeLast*LOG_GiftAvgLast 1 -0.0136 0.00265 26.42 <.0001 0.986

GiftTimeLast*LOG_GiftCntCard36 1 -0.0239 0.00695 11.86 0.0006 0.976

IMP_DemAge*LOG_GiftCntCard36 1 0.0114 0.00202 32.02 <.0001 1.012

IMP_DemAge*PromCntCardAll 1 -0.00032 0.000092 12.23 0.0005 1.000

Unfortunately, all but one of the selected terms is an

interaction.

While this model is the best predictor of PVA97NK response

found up to this time, it is nearly impossible to interpret. This is an

important factor to remember when considering polynomial regression models.

Exercises

Predictive Modeling Using

Regression

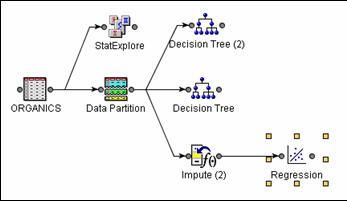

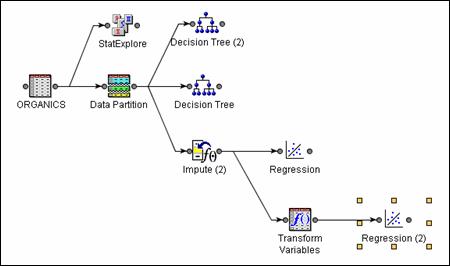

Return to the Chapter 4 Organics diagram in the Exercises project.

Explore the ORGANICS data source.

In preparation for regression, is any missing values imputation needed?

If yes, should you do this imputation before generating the decision tree

models? Why or why not?

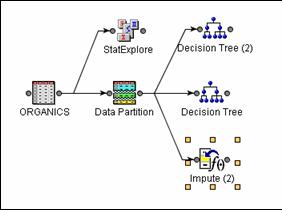

Add an Impute node to the diagram and connect it to the Data Partition

node.

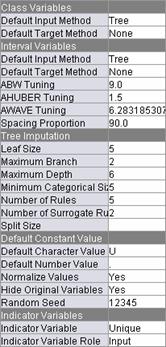

Change Default Input Method to Tree for both class and interval

variables. Create missing value indicator variables. Replace missing values for

GENDER with U for unknown.

Add a Regression node to the diagram and connect it to the Impute node.

Choose the stepwise selection and average squared error as the

selection criterion.

Run the Regression node and view the results. Which variables are

included in the final model? Which variables are important in this model?

In preparation for regression, are any transformations of the data

warranted? Why or why not?

Add a Transform Variables node to the diagram and connect it to the

Impute node.

The variable AFFL appears to be skewed to the

right. Use a square root transformation for AFFL. The variables BILL and LTIME also appear to be skewed to

the right. Use SAS Enterprise Miner to transform these variables to maximize

normality.

Run the Transform Variables node. Explore the exported training data.

Did the transformation of AFFL appear to result in a less

skewed distribution? What transformation was chosen for the variables BILL and LTIME

Add another Regression node to the diagram and connect it to the Transform

Variables node.

Choose the stepwise selection method and average squared error

selection criterion.

Run this new Regression node and view the results. Which variables are

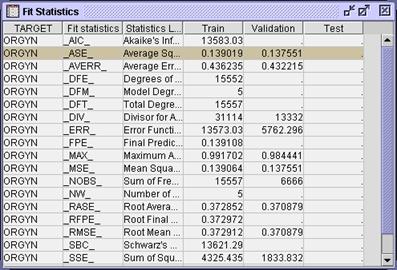

included in the final model? Which variables are important in the model?

How do the validation average squared errors of the two regression

models compare? How do the regression models compare to the tree models?

Regression

models are a prolific and useful way to create predictions. New cases are

scored using a prediction formula. Inputs are selected via a sequential selection

process. Model complexity is controlled by fit statistics calculated on

validation data.

To

use regression models, there are several issues with which to contend that go

beyond the predictive modeling essentials. First, a mechanism for handling missing

input values must be included in the model development process. Second, methods

for handling extreme or outlying predictions should be included. Third, the

level-count of a categorical should be reduced to avoid overfitting. Finally,

the model complexity might need to be increased beyond what is provided by

standard regression methods. One approach to this is polynomial regression.

Polynomial regression models can be fit by hand with specific

interactions in mind. They also can be fit autonomously by selecting polynomial

terms from a list of all polynomial candidates.

Predictive

Modeling Using Regression

Right-click

the ORGANICS data source in

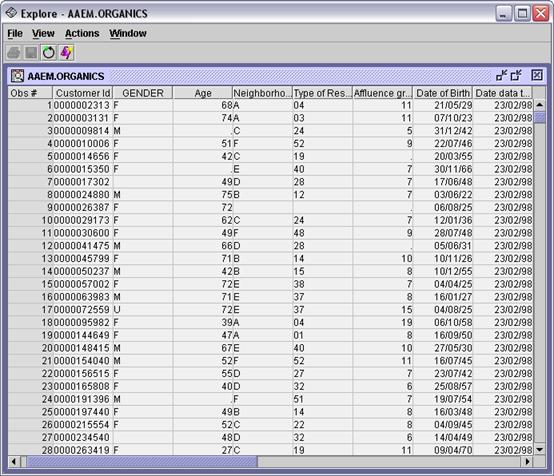

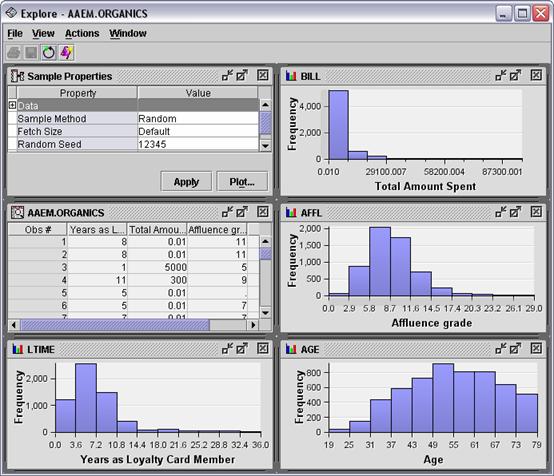

the Project Panel and select Explore.

Examine

the ORGANICS data table to reveal several

inputs with missing values. A more precise way to determine the extent of

missing values in this data set is to use the StatExplore node.

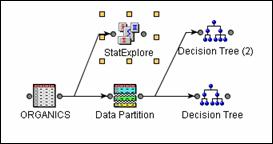

Connect

a StatExplore node to the ORGANICS data source in the diagram workspace.

Select

the StatExplore node in the

diagram and examine the Properties panel.

Change

the option to Hide Rejected Variables to No

and change the option for Interval Variables to Yes using the menus.

Run

the StatExplore node and examine the Output window in the Results.

Class

Variable Summary Statistics

(maximum

500 observations printed)

Variable Role Numcat NMiss Mode

CLASS INPUT 4 0 Silver

GENDER INPUT 4 2512 F

NGROUP INPUT 8 674 C

REGION INPUT 6 465 South East

TV_REG INPUT 14 465 London

ORGYN TARGET 2 0 0

The variable GENDER has a

relatively large number of missing values.

Interval Variable Summary

Statistics

(maximum 500 variables

printed)

Variable ROLE Mean StdDev Non Missing Missing

AFFL INPUT 9 3 21138 1085

AGE INPUT 54 13 20715 1508

BILL INPUT 4421 7559 22223 0

LTIME INPUT 7 5 21942 281

The variables AFFL and AGE have

over 1000 missing values each.

Imputation

of missing values should be done prior to generating a regression model.

However, imputation is not necessary before generating a decision tree

model because a decision tree can use missing values in the same way as any other

data value in the data set.

Close the

StatExplore node results and return to the diagram workspace.

After you

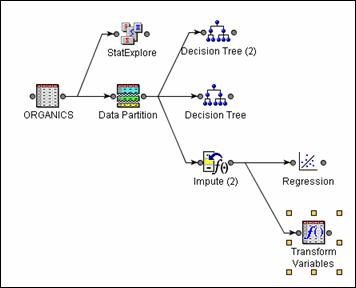

add an Impute node, the diagram should appear as shown below.

Choose

the imputation methods.

Select

the Impute node in the

diagram.

To

use tree imputation as the default method of imputation, change the Default

Input Method for both class and interval variables to Tree using the menus.

To create

missing value indicator variables, change the Indicator Variable property to Unique

and the Indicator Variable Role to Input using the menus in the Properties panel.

To replace

missing values for the variable GENDER with U, first change Default Character Value to U. The Properties panel

should appear as shown.

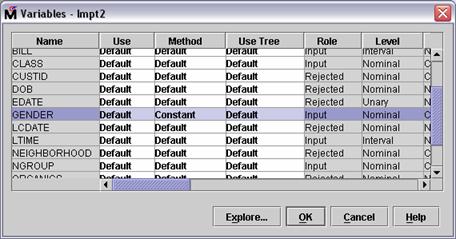

Select Variables . . Change the value in

the Method column for the variable GENDER to Constant as shown below.

Select OK to confirm the change.

Add a Regression node to the

diagram as shown below.

Choose

the stepwise selection and average squared error as the selection criterion.

Select

the Regression node in the

diagram.

Select

Selection Model Stepwise.

Select

Selection Criterion Validation

Error.

Run the

Regression node and view the results. The Output window shows which variables

are in the final model and which variables are important.

Line

658 lists the inputs included in the final model:

Intercept IMP_AFFL IMP_AGE IMP_GENDER M_AFFL M_AGE M_GENDER

Important

inputs can be ascertained by Wald Chi-Square, standardized estimates, and odds

ratio estimates.

Analysis of Maximum Likelihood

Estimates

Standard Wald Standardized

Parameter DF Estimate Error Chi-Square Pr > ChiSq Estimate Exp(Est)

Intercept 1 -0.7674 0.1336 33.01 <.0001 0.464

IMP_AFFL 1 0.2513 0.00721 1215.16 <.0001 0.4637 1.286

IMP_AGE 1 -0.0534 0.00179 895.19 <.0001 -0.3786 0.948

IMP_GENDER

F 1 0.9688 0.0480 407.57 <.0001 2.635

IMP_GENDER

M 1 0.0485 0.0528 0.84 0.3584 1.050

M_AFFL 0 1 -0.1276 0.0464 7.56 0.0060 0.880

M_AGE 0 1 -0.1051 0.0408 6.63 0.0100 0.900

M_GENDER 0 1 -0.2324 0.0767 9.18 0.0024 0.793

Odds Ratio Estimates

Point

Effect Estimate

IMP_AFFL 1.286

IMP_AGE 0.948

IMP_GENDER

F vs U 7.287

IMP_GENDER

M vs U 2.903

M_AFFL 0 vs 1 0.775

M_AGE 0 vs

1 0.810

M_GENDER 0 vs 1 0.628

Important inputs include IMP_AFFL IMP_AGE, and IMP_GENDER

Close the

regression results and return to the diagram workspace.

Explore

the input distributions.

Select the ORGANICS node and select Variables . in the Properties

panel.

Select all interval input

variables.

Select Explore . .

The variables AFFL BILL, and LTIME are skewed to the right and

might need to be transformed for a regression. This is evident in the

histograms that can be viewed in the exploration tool available in the Input

Data node and other nodes.

Connect a Transform Variables node as shown below.

Transform inputs.

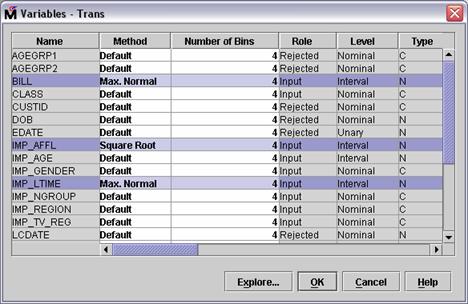

Select Variables . in the Transform Variables node's Properties panel.

In the Method column for the

variable IMP_AFFL, select Square

Root from the menu. In the Method column for the variables BILL and IMP_LTIME, select Max. Normal from the menu. The

Variables window should appear as shown below.

Select OK

to confirm the changes.

Run the Transform Variables node. Do not view the results. Instead,

select Exported Data . from

the Transform Variables node's Properties panel. The Exported Data - Transform

Variables window opens.

Select the Train data set and select Explore . .

In the

Explore window, select Actions

Plot . .

Select Histogram as the

type of chart and then select Next >.

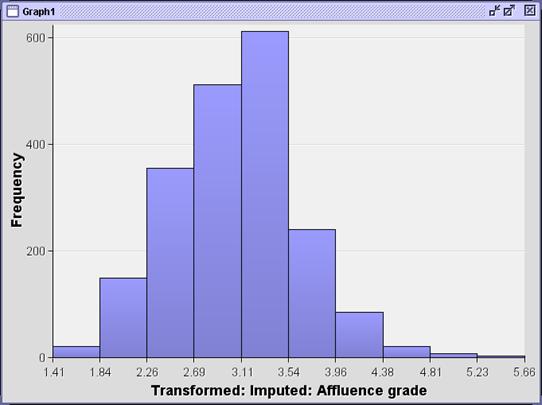

Change the role of SQRT_IMP_AFFL to X.

Select Finish.

The

transformed variable appears to be less skewed than the original variable.

To view the transformations for the other variables,

close the graph and examine the Transformations window in the results. The

transformation chosen for the variable BILL was a square root transformation, and the

transformation for IMP_LTIME was the fourth root. You can confirm this by

opening the Results window and viewing lines 28-25 of the output.

Transformations

(Maximum 500 observations printed)

Input Input Output

Name Role Level Output Name Level Formula

BILL INPUT INTERVAL SQRT_BILL INTERVAL Sqrt(_SCALEVAR_)

IMP_AFFL INPUT INTERVAL SQRT_IMP_AFFL INTERVAL Sqrt(IMP_AFFL + 1)